Monex Global Retail Investor Survey Report

December 2020

Summary

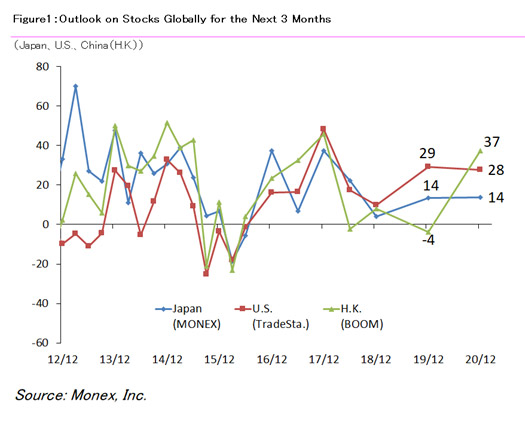

Summary [The forecast DI for world stock markets]

[Japan]

|

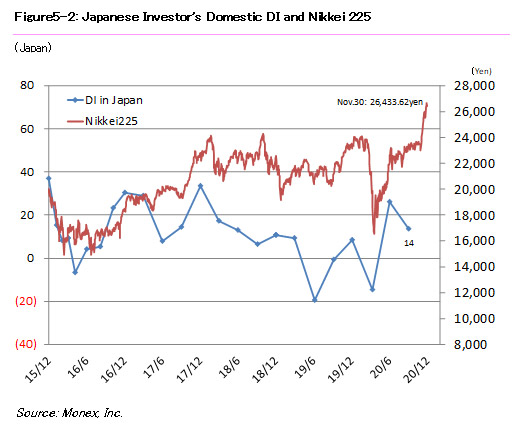

Dec. 2019: 14 → Dec. 2020: 14 (±0 points)

|

[U.S.]

|

Dec. 2019: 29 → Dec. 2020: 28 (-1 points)

|

[China (H.K.)]

|

Dec. 2019:-4 → Dec. 2020: 37 (+41 points)

|

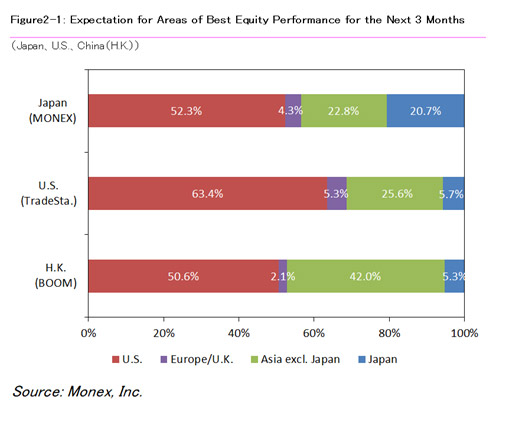

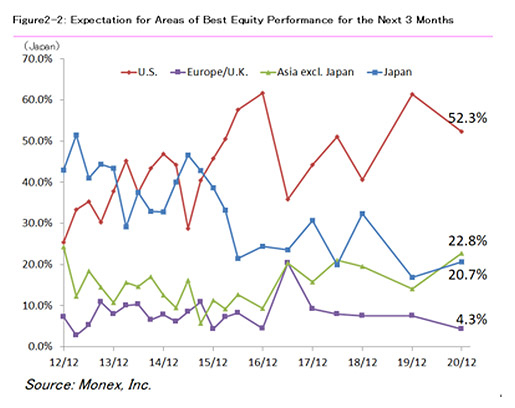

[Expectations for stock markets in the coming three months]

[Japan]

|

U.S.: 52.3%

|

Europe/U.K.: 4.3%

|

Asia excl. Japan: 22.8%

|

Japan: 20.7%

|

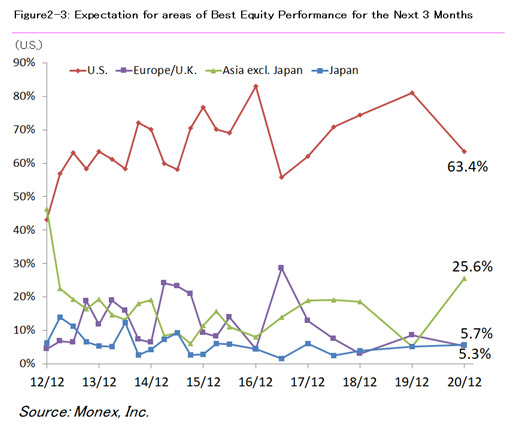

[U.S.]

|

U.S.: 63.4%

|

Europe/U.K.: 5.3%

|

Asia excl. Japan: 25.6%

|

Japan: 5.7%

|

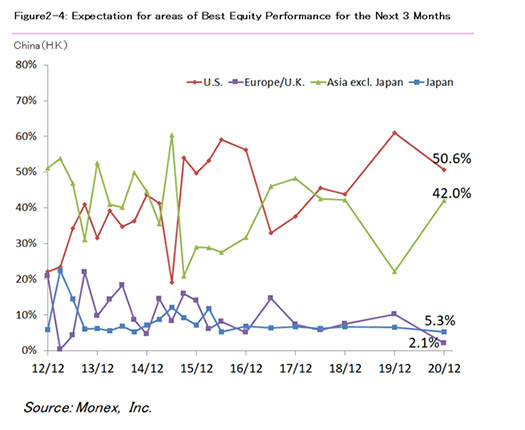

[China (H.K.)]

|

U.S.: 50.6%

|

Europe/U.K.: 2.1%

|

Asia excl. Japan: 42.0%

|

Japan: 5.3%

|

Results

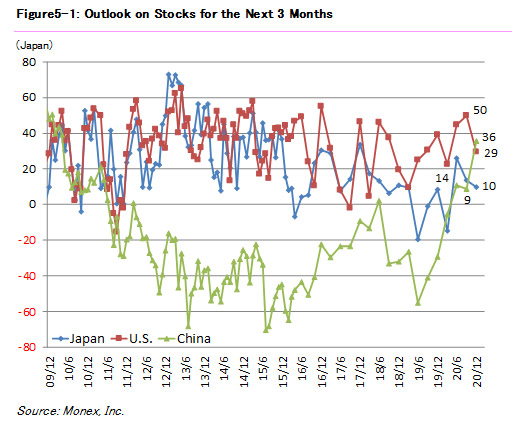

Results [Japanese Stocks DI]

|

Sep. 2020: 14 → Dec. 2020: 10 (-4 points)

|

[U.S. Stocks DI]

|

Sep. 2020: 50 → Dec. 2020: 29 (-21 points)

|

[China stocks DI]

|

Sep. 2020: 9 → Dec. 2020: 36 (+27points)

|

Japan

Method:

|

Online survey

|

Respondents:

|

Customers of Monex, Inc.

|

# of Responses:

|

1,006

|

Period:

|

Nov. 19 to Nov. 30, 2020

|

United States

Method:

|

Online survey

|

Respondents:

|

Customers of TradeStation Securities, Inc.

|

# of Responses:

|

777

|

Period:

|

Nov. 19 to Nov. 30, 2020

|

Hong Kong

Method:

|

Online survey

|

Respondents:

|

Customers of Monex Boom Securities (H.K.) Limited

|

# of Responses:

|

474

|

Period:

|

Nov. 23 to Nov. 30, 2020.

|

Disclaimer

The Monex Global Retail Investor Survey measures customer sentiment based upon answers to specific questions received from a random sampling of customers of Monex, Inc., TradeStation Securities, Inc. and Monex Boom Securities (H.K.) Limited. Details of the methodology used to conduct the survey are available upon request. Accuracy and completeness of the data derived from the survey are not guaranteed.